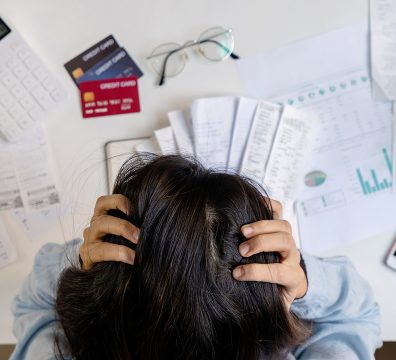

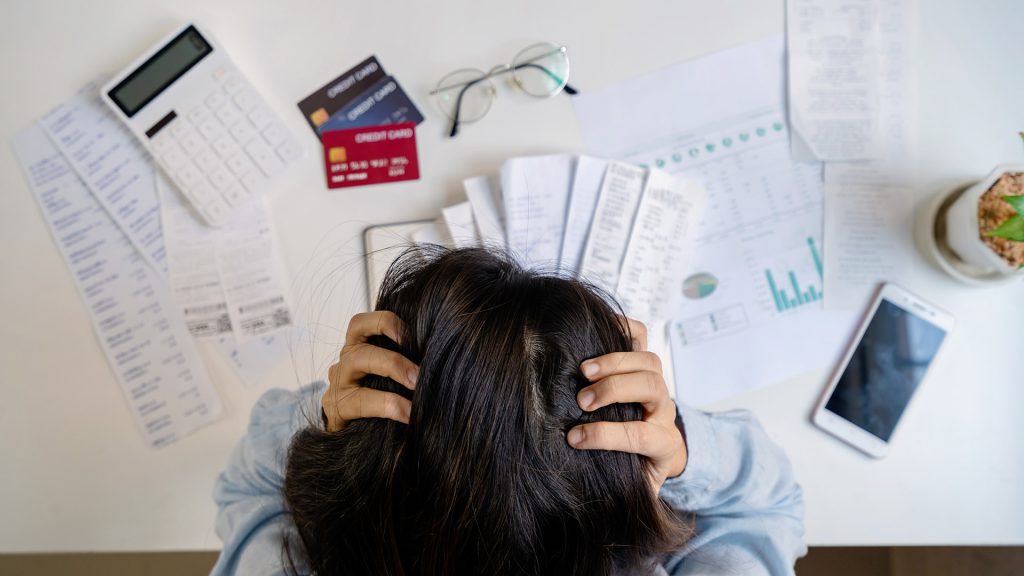

Many Albertans are feeling the pinch of inflation, higher interest rates and growing debt balances. Credit cards, lines of credit, and personal loans can add up fast, especially when each carries a different interest rate. One effective strategy to simplify and potentially reduce these costs is debt consolidation through mortgage refinancing. But before you take this step, it’s important to understand how it works and whether it’s right for your situation.

What Is Debt Consolidation Through Refinancing?

Debt consolidation through refinancing means using the equity in your home to pay off higher-interest debts. Essentially, you replace your current mortgage with a new, larger one that includes your existing mortgage balance plus the debts you want to consolidate. The goal is to have one monthly payment at a lower interest rate.

For example, if your home in Lethbridge or Calgary has increased in value since you bought it, you may be able to access up to 80% of your home’s current appraised value through refinancing (as allowed under Canadian mortgage rules).

Benefits for Alberta Homeowners

- Lower Interest Costs: Credit cards often carry rates above 20%, while mortgage rates (despite recent fluctuations), remain significantly lower.

- Simplified Payments: One payment instead of several reduces the chance of missed due dates and late fees.

- Improved Cash Flow: Lower monthly payments can free up room in your budget.

- Potential Credit Boost: Paying down high-interest debts can improve your credit utilization ratio over time.

Things to Consider Before Refinancing

Refinancing isn’t always the right move for everyone. Here’s what to weigh carefully:

- Penalties: If you’re breaking your existing mortgage term early, your lender may charge a prepayment penalty.

- Longer Amortization: Extending your mortgage term may reduce your monthly payment but increase your total interest over time.

- Qualification Rules: You’ll still need to meet the lender’s stress test and income verification requirements under the federal OSFI guidelines.

- Equity Requirements: You typically need at least 20% equity remaining in your home after refinancing.

- Behavioral Changes: Consolidating debt can be a helpful reset, but it won’t solve the problem if spending habits don’t change. Without careful budgeting, it’s easy to build credit card balances back up again.

Is It the Right Move for You?

If your unsecured debt is high and your home’s value has grown, refinancing could be a smart way to regain control. However, it’s best to work with a licensed Alberta mortgage broker like Chris Marriner who can assess your full financial picture and compare refinancing options from multiple lenders—not just your bank.

A broker can also help you decide whether a refinance, home equity line of credit (HELOC), or second mortgage makes the most sense based on your long-term goals.

Final Thoughts

Debt consolidation through mortgage refinancing can provide breathing room and reduce financial stress, but it’s not a one-size-fits-all solution. The key is understanding the costs, benefits, and future impact on your home equity. If you’re considering this route, talk to Chris Marriner, Mortgage broker who can guide you through the numbers before making any commitments.